Author: CA Devesh Thakur

Category: GST Basics | 30 Days GST Challenge – Day 5

Introduction

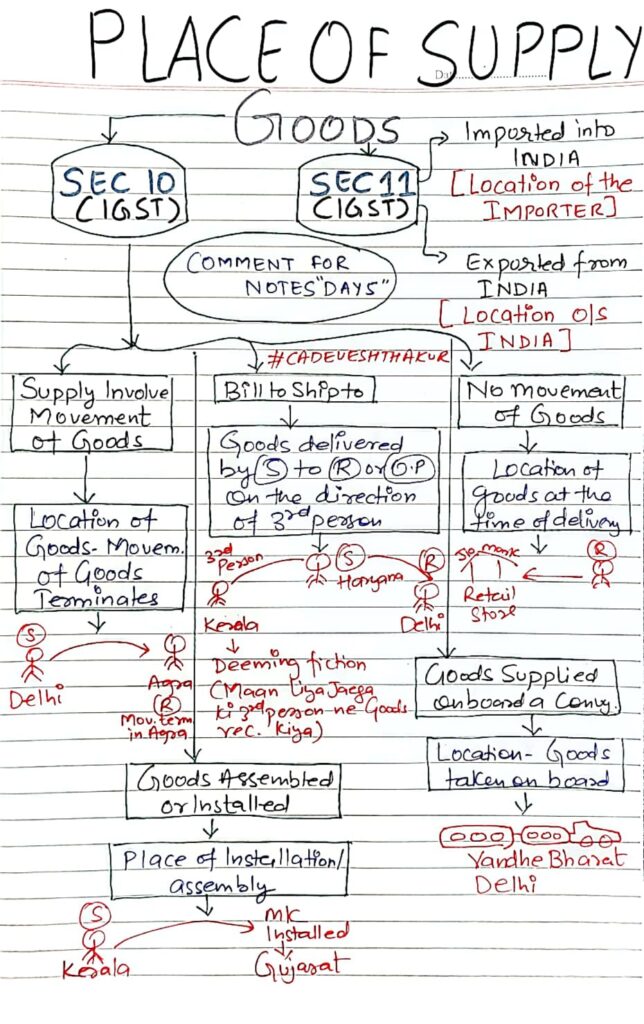

The concept of Place of Supply plays a crucial role in determining whether a supply is inter-state or intra-state, which further affects whether IGST or CGST & SGST will be levied. For goods, this is governed by Sections 10 and 11 of the IGST Act.

Let’s decode these sections with practical illustrations.

Applicable Provisions: Sec 10 & Sec 11 of IGST Act

Section 10 – When the supply of goods is within India

This section applies when both supplier and recipient are located in India.

Section 11 – When the supply of goods involves import/export

This section deals with supplies where either the supplier or recipient is located outside India.

Section 10 – Detailed Scenarios and Examples

Movement of Goods by Supplier, Recipient or Other Person

Provision:

If the supply involves movement of goods (by the supplier, recipient, or any other person), the place of supply is the location where movement terminates for delivery.

Example:

- Supplier (S) in Delhi sends goods to recipient (R) in Agra.

- Movement terminates in Agra.

Place of Supply: Agra (Uttar Pradesh)

Inter-State Supply – IGST Applicable

“Bill To – Ship To” Scenario

Provision:

When goods are delivered by the supplier to a third person on the direction of the buyer (deemed recipient), the place of supply is the location of the person who gave the direction.

Example:

- Buyer (3rd Person) in Kerala instructs Seller (S) in Haryana to deliver goods directly to another recipient (R) in Delhi.

- Though goods are delivered to Delhi, they are billed to Kerala.

Place of Supply: Kerala

Deemed that 3rd person has received the goods

No Movement of Goods

Provision:

When there is no movement of goods, the place of supply is the location of the goods at the time of delivery.

Example:

- Goods picked up by buyer from a retail store in Delhi.

Place of Supply: Delhi

Intra-State Supply – CGST + SGST Applicable

Goods Installed or Assembled at Site

Provision:

If goods are supplied and are to be installed or assembled at a site, the place of supply is the place of installation/assembly.

Example:

- Machinery sent from Kerala and installed in Gujarat.

Place of Supply: Gujarat

Tax determined based on location of installation

Goods Supplied on Board a Conveyance

Provision:

Where goods are supplied on board a conveyance (e.g. train, aircraft, vessel), the place of supply is the location at which such goods are taken on board.

Example:

- Goods supplied on Vande Bharat train while boarding in Delhi.

Place of Supply: Delhi

Section 11 – Import and Export of Goods

Goods Imported into India

Provision:

Place of supply for imports is the location of the importer.

Example:

- Goods imported by a company in Mumbai.

Place of Supply: Mumbai

Goods Exported from India

Provision:

Place of supply for exports is outside India, but for GST compliance, it is deemed to be the location outside India.

Example:

- Goods exported from Delhi to the USA.

Place of Supply: USA (outside India)

Export – Zero-Rated Supply

Summary

| Scenario | Section | Place of Supply | Example |

| Movement of goods | Sec 10 | Place where movement terminates | Delhi → Agra → Agra |

| Bill to – Ship to | Sec 10 | Location of the person who ordered | Kerala orders, ship to Delhi → Kerala |

| No movement of goods | Sec 10 | Location at time of delivery | Picked from Delhi retail store → Delhi |

| Goods installed/assembled | Sec 10 | Place of installation/assembly | Installed in Gujarat → Gujarat |

| Supplied on a conveyance | Sec 10 | Location where goods taken on board | Vande Bharat, boarded in Delhi → Delhi |

| Import of goods | Sec 11 | Location of importer | Importer in Mumbai → Mumbai |

| Export of goods | Sec 11 | Outside India | Export to USA → Outside India |

Conclusion

Understanding the Place of Supply is key to determining the correct GST liability. Whether you’re a trader, manufacturer, or a service provider dealing in goods, a correct classification under Section 10 or 11 of the IGST Act can ensure compliance and smooth business operations.

")

{kind=link}